")

Introduction

Many high school students graduate without understanding how to create a budget, manage debt, or make informed financial decisions. This gap in financial education can lead to costly mistakes in early adulthood, from overwhelming student loans to poor credit management. The National Personal Finance Challenge addresses this critical need by transforming money education into an engaging, competitive learning experience that prepares students for real-world financial decisions.

Financial literacy competitions like the NPFC provide structured opportunities for students to develop practical money skills in a supportive environment. Rather than passively absorbing information, participants actively apply concepts through quiz-based challenges that test their understanding of budgeting, saving, investing, and responsible financial decision-making.

Why the National Personal Finance Challenge Matters

Financial education in U.S. schools remains inconsistent across states, leaving many students unprepared for financial independence. The National Personal Finance Challenge fills this educational gap by providing a standardized framework for learning essential money management concepts.

Students who participate in structured financial education programs demonstrate stronger decision-making skills when facing real financial choices. They’re more likely to create emergency funds, avoid high-interest debt, and understand the long-term impact of compound interest on savings and loans. These competitions make abstract financial concepts concrete by presenting scenarios students will actually encounter: choosing between job offers with different benefit packages, understanding credit card terms, or deciding between renting and saving for a down payment.

The challenge format encourages teamwork and critical thinking. Students learn to evaluate financial information quickly, identify misleading marketing claims, and apply mathematical reasoning to money decisions. These skills extend beyond personal finance into broader areas of consumer protection and economic literacy.

Early exposure to financial literacy helps students develop informed money habits and avoid common financial mistakes later in life.

What Is the National Personal Finance Challenge?

The National Personal Finance Challenge is a quiz-bowl style academic competition focused on personal finance knowledge and application. Teams of high school students compete by answering questions across multiple categories of financial literacy, from basic budgeting concepts to more complex topics like investment diversification and tax fundamentals.

The competition structure typically includes individual testing rounds and team-based question sessions. Students face scenarios requiring them to calculate interest rates, compare financial products, identify appropriate insurance coverage, and evaluate economic trends. The format rewards both quick recall of financial facts and deeper analytical thinking about money management strategies.

Participation is open to high school students nationwide, usually organized through schools or youth organizations. The challenge serves as both a learning tool and a recognition program for students developing strong financial capabilities.

How the National Personal Finance Challenge Builds Real-World Money Skills

The National Personal Finance Challenge helps students turn financial concepts into practical decision-making skills. By working through realistic scenarios, participants learn how budgeting, saving, credit management, and basic investing apply to everyday life.

The competitive format encourages critical thinking and teamwork, requiring students to evaluate financial choices quickly and accurately. This hands-on approach strengthens financial judgment and builds confidence, preparing students to manage real-world money decisions responsibly.

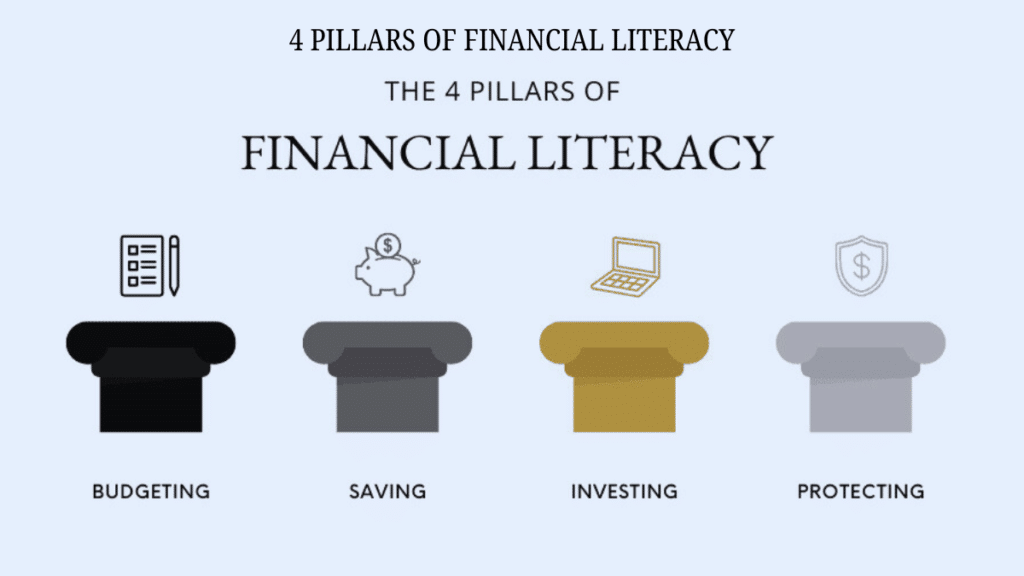

Core Financial Concepts Tested in NPFC

The 4 Pillars of Financial Literacy

Understanding personal finance rests on four foundational pillars that every student should master:

Earning involves understanding income sources, employment compensation, tax withholdings, and career financial planning. Students learn to evaluate job offers based on total compensation, not just hourly wages, considering benefits like health insurance and retirement contributions.

Spending focuses on budgeting, tracking expenses, distinguishing needs from wants, and making informed consumer decisions. This pillar teaches students to recognize marketing tactics, compare prices effectively, and avoid impulse purchases that derail financial goals.

Saving emphasizes building emergency funds, setting financial goals, and understanding different savings vehicles. Students learn why keeping three to six months of expenses in accessible savings protects against unexpected job loss or medical emergencies.

Investing introduces long-term wealth building through retirement accounts, index funds, and understanding risk tolerance. The focus remains on foundational concepts like compound growth, diversification, and time horizon rather than speculative trading strategies.

The 5 C’s of Personal Finance

Financial institutions and educators often reference five critical components of personal financial management:

Character reflects your credit history and payment reliability. Lenders evaluate whether you’ve consistently met previous financial obligations.

Capacity measures your ability to repay debt based on income versus existing obligations. The debt-to-income ratio helps determine sustainable borrowing levels.

Capital represents your current financial resources, including savings, investments, and valuable assets that could support loan repayment if needed.

Collateral includes assets pledged as security for loans, particularly relevant for mortgages and auto loans where the purchased item secures the debt.

Conditions encompass economic factors affecting your financial situation, from interest rate environments to industry-specific employment trends.

Essential Money Rules Students Learn

Financial education competitions introduce students to practical frameworks that simplify complex money decisions:

The 70/20/10 Rule provides a straightforward budgeting approach: allocate 70% of after-tax income to living expenses and discretionary spending, direct 20% toward savings and debt repayment, and dedicate 10% to charitable giving or additional savings goals. While individual circumstances vary, this framework helps students think proportionally about money allocation.

The Rule of 7 demonstrates compound interest’s power by estimating how long money takes to double. Dividing 72 by the annual interest rate approximates the doubling period. At a 7% average annual return, an investment doubles in roughly 10 years. This concept helps students understand why starting retirement savings early creates substantial long-term advantages.

Students also explore emergency fund logic, learning why financial experts recommend saving three to six months of essential expenses. This buffer provides security during job transitions, medical emergencies, or unexpected major repairs without forcing reliance on high-interest credit cards.

The Rule of 7 helps students understand how compound interest allows money to grow over time by earning returns on both the original amount and previously earned interest.

Benefits & Limitations of Financial Education Competitions

| Benefits | Limitations |

| Structured learning with clear educational objectives | Competition format may not suit all learning styles |

| Practical application of theoretical concepts | Focus on testable knowledge may oversimplify complex decisions |

| Team collaboration develops communication skills | Time constraints don’t reflect real financial decision timelines |

| Recognition motivates continued financial education | Quiz format can’t fully replicate emotional aspects of money management |

| Exposure to diverse financial scenarios | May not address individual cultural or family financial contexts |

Understanding these limitations helps students and educators use competitions as one component of comprehensive financial education rather than a complete solution.

Common Mistakes Students Make

Even motivated students encounter predictable challenges when learning personal finance concepts:

Confusing saving and investing leads to inappropriate risk-taking with emergency funds or excessive conservatism with long-term retirement money. Students need clear guidance on matching financial tools to specific goals and timelines.

Overestimating investment returns creates unrealistic expectations. While historical stock market averages suggest 7-10% annual returns over decades, students must understand volatility, inflation’s impact, and the difference between nominal and real returns.

Underestimating compound debt works against financial health just as compound interest works for savings. Credit card balances carrying 18-25% interest rates can double surprisingly quickly when making only minimum payments.

Ignoring risk management leaves students vulnerable to preventable financial catastrophes. Understanding basic insurance principles—health, auto, renters—protects against expenses that could eliminate years of careful saving.

Practical Learning Tips for Students & Educators

Effective preparation for financial literacy competitions requires consistent, applied learning rather than last-minute cramming:

Start with real scenarios from your own life. Track personal spending for a month, calculate the true cost of a car including insurance and maintenance, or compare college financing options. Concrete examples make abstract principles memorable.

Use calculation practice to build comfort with financial math. Regular practice with compound interest formulas, budget percentages, and debt payoff calculations develops speed and accuracy.

Review financial news critically to understand current economic conditions. Identify how interest rate changes affect borrowing costs, how inflation impacts purchasing power, or how employment trends influence career planning.

Leverage technology thoughtfully when learning. AI tools can explain complex financial concepts, generate practice questions, or check mathematical calculations. However, students should verify AI-generated financial information against authoritative sources and develop independent analytical skills rather than relying on automated answers.

Frequently Asked Questions

Q1. What are the main challenges of personal finance?

The primary challenges include limited financial education in schools, complex financial products with unclear terms, emotional spending decisions, and difficulty balancing competing financial priorities like debt repayment versus retirement saving.

Q2. What is NPFC?

NPFC stands for National Personal Finance Challenge, a competitive academic program where high school students test their knowledge of budgeting, saving, investing, credit management, and economic principles through quiz-bowl style questions.

Q3. What are the 4 pillars of financial literacy?

The four pillars are earning, spending, saving, and investing. These categories encompass all major aspects of personal money management from generating income through building long-term wealth.

Q4. What is the 70/20/10 rule of money?

This budgeting guideline suggests allocating 70% of after-tax income to expenses, 20% to savings and debt reduction, and 10% to charitable giving or additional savings. Individual circumstances may require adjustments to these percentages.

Q5. How can students use AI for personal finance learning?

AI tools can explain financial concepts, generate practice scenarios, perform calculations, and identify knowledge gaps. Students should verify AI-provided financial information against trusted sources and use these tools to enhance, not replace, critical thinking about money decisions.

Q6. What makes a good emergency fund?

An effective emergency fund covers three to six months of essential expenses, remains easily accessible in a savings account, and serves exclusively for unexpected financial emergencies like job loss or major medical expenses.

Q7. How does compound interest affect student loans?

Compound interest on student loans means interest charges accrue on both the original loan amount and previously accumulated interest. This effect makes loan balances grow faster, particularly during deferment periods, emphasizing the importance of understanding loan terms before borrowing.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Students and families should consult qualified financial professionals when making significant financial decisions.