You’ve built equity in your rental property over the years. Now you’re eyeing another investment opportunity or need cash for major renovations, but you don’t want to sell. This is where an investment property equity line of credit becomes relevant. It’s essentially a way to tap into your property’s value without giving up ownership. But unlike your primary residence, getting a line of credit on an investment property comes with different rules, higher rates, and specific risks. This guide breaks down exactly how it works, what it costs, who should consider it, and the mistakes that trip up most beginners.

What Investment Property Equity Line of Credit Really Means in Everyday Investing

Definition & Meaning

An investment property equity line of credit, often called an investment property HELOC, is a revolving credit line secured by the equity you’ve built in a rental or investment property. Think of it like a credit card, but instead of an unsecured limit, your property acts as collateral. You can borrow up to a certain amount during what’s called the draw period, pay it back, and borrow again if needed. The key difference from a regular HELOC is that this one is tied to a non-owner-occupied property, which makes lenders more cautious.

Equity in Investment Property Explained

Equity is simply the portion of your property you actually own outright. If your rental property is worth $400,000 and you owe $250,000 on the mortgage, you have $150,000 in equity. Lenders typically let you borrow against a percentage of that equity. For investment properties, most banks cap it at 75% to 80% of the property’s value, minus what you still owe. So in this example, if the lender allows 75% loan-to-value (LTV), you’d multiply $400,000 by 0.75 to get $300,000. Subtract your $250,000 mortgage, and you could access up to $50,000 through a HELOC.

Difference Between HELOC & Home Equity Loan

Both let you borrow against equity, but they work differently. A home equity loan gives you a lump sum upfront with fixed monthly payments over a set term, like a second mortgage. An investment property equity line of credit is flexible—you draw what you need when you need it during the draw period (usually 5-10 years), and you only pay interest on what you actually use. After the draw period ends, you enter repayment mode where you can’t borrow more and must pay back principal plus interest. For investors who need ongoing access to cash for multiple projects or unpredictable expenses, the HELOC structure usually makes more sense.

How Investment Property Equity Line of Credit Works Step by Step (Real-Life Flow)

Calculating Available Equity

Before applying, figure out what you can realistically access. Get a rough idea of your property’s current market value—you can use online tools like Zillow or Redfin, but lenders will require a professional appraisal. Multiply that value by the lender’s maximum LTV ratio for investment properties (commonly 75%). Then subtract your remaining mortgage balance. That’s your potential credit line. Keep in mind lenders also consider your debt-to-income ratio and credit score, so even if the math works, approval isn’t guaranteed.

Applying for the Line of Credit

The application process mirrors getting a mortgage but with stricter requirements for investment properties. You’ll need to provide recent tax returns, rental income documentation, credit reports, property appraisals, and proof of cash reserves. Lenders want to see that the property generates positive cash flow and that you can handle payments even if it sits vacant for a few months. Expect the underwriting process to take 30-45 days. Because these loans carry more risk for lenders, approval standards are tighter than for primary residence HELOCs.

Draw Periods & Repayment

During the draw period, you access funds as needed up to your credit limit. Most lenders provide checks, a card, or online transfers. You typically pay only interest during this phase, which keeps monthly payments low but doesn’t reduce your principal balance. Once the draw period ends—say, after 10 years—you enter the repayment period (often 15-20 years). Now you can’t borrow anymore, and payments include both principal and interest, which usually makes them significantly higher. Some people get caught off guard by this jump.

Common Lender Requirements

Most lenders require a minimum credit score of 680-700 for investment property HELOCs, though some prefer 720 or higher. You’ll need at least 20-25% equity in the property. Debt-to-income ratios should generally stay below 43%, though some lenders allow up to 50% if other factors are strong. Cash reserves covering 6-12 months of mortgage payments are often required. The property must be in good condition—lenders won’t approve a HELOC on a fixer-upper until repairs are complete. And expect higher interest rates than you’d get on a primary residence HELOC, often 1-2 percentage points more.

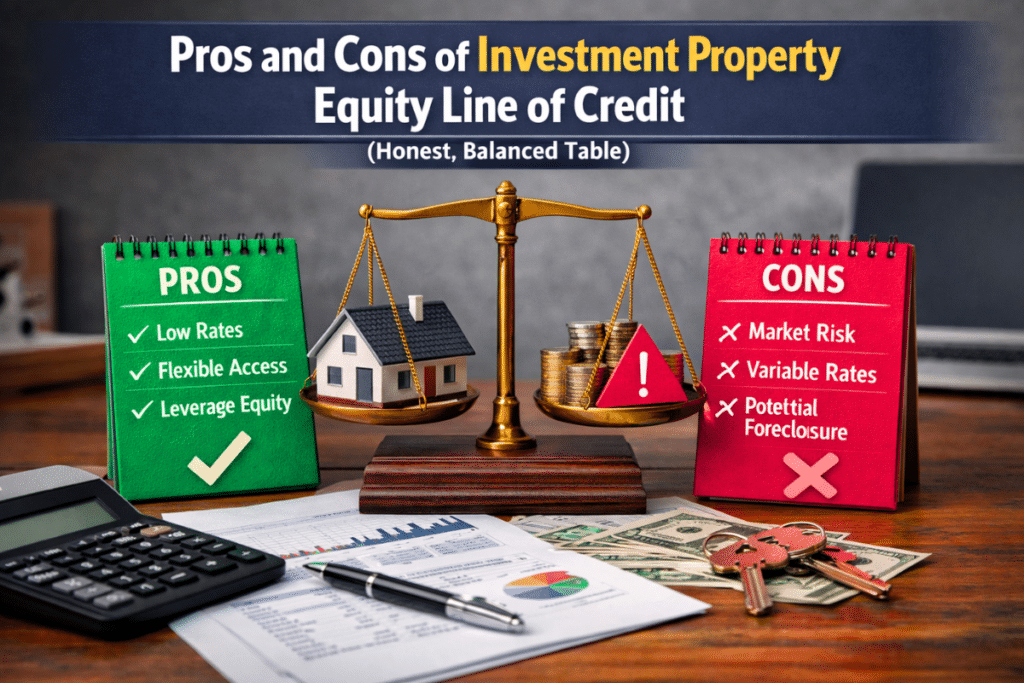

Pros and Cons of Investment Property Equity Line of Credit (Honest, Balanced Table)

| Pros | Cons |

| Access cash without selling the property | Higher interest rates than primary residence HELOCs |

| Flexibility to borrow only what you need | Variable rates can increase your payments unpredictably |

| Interest may be tax-deductible if used for property improvements | Stricter qualification requirements |

| Can fund renovations that increase property value | Risk of foreclosure if you can’t make payments |

| Useful for purchasing additional investment properties | Closing costs and fees (often 2-5% of credit line) |

| Only pay interest on what you use during draw period | Payment shock when repayment period begins |

| Revolving credit lets you reuse paid-back funds | Reduced equity means less cushion if property values drop |

The table makes it clear: this tool offers real advantages for experienced investors who understand leverage, but it amplifies risk for beginners who might overextend themselves or underestimate how quickly variable rates can climb.

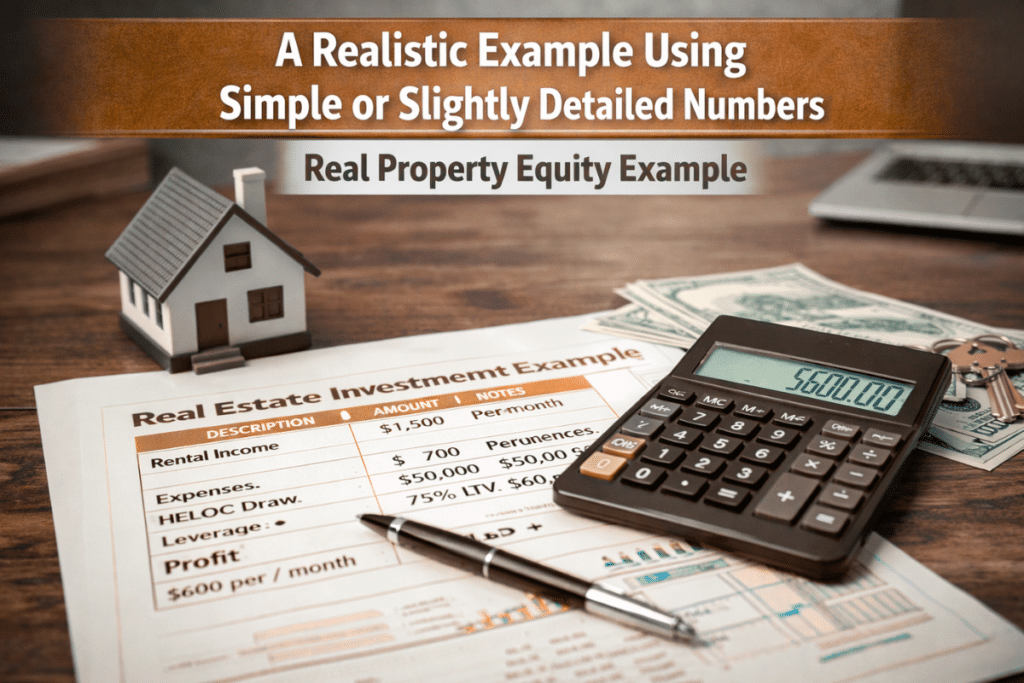

A Realistic Example Using Simple or Slightly Detailed Numbers

Example #1 – Renovation Funding

Let’s say you own a duplex worth $350,000 with a $200,000 mortgage balance. You have $150,000 in equity. Your lender offers a HELOC at 75% LTV, which means they’ll lend up to $262,500 (75% of $350,000). Subtract your mortgage of $200,000, and you can access $62,500. You decide to use $40,000 to renovate one unit—new kitchen, updated bathroom, fresh paint. The renovations increase the property’s value to $385,000 and let you raise rent by $300 per month. During the 10-year draw period, you pay interest-only on the $40,000 at a variable rate currently sitting at 8.5%. That’s about $283 per month. The extra rental income covers this payment and adds to your cash flow. When the repayment period starts, you’ll pay principal plus interest, but by then the property’s worth more and generates higher income.

Example #2 – Leveraging Equity to Buy New Property

You have a rental property worth $500,000 with $150,000 still owed. At 75% LTV, you can access about $225,000 ($500,000 × 0.75 = $375,000 minus $150,000 mortgage). You use $80,000 as a down payment on a second rental property priced at $320,000. This lets you expand your portfolio without liquidating savings or selling your existing property. The second property generates $2,400 monthly rent. After mortgage, insurance, taxes, and maintenance, it nets about $600 per month. Your HELOC payment on $80,000 at 8% interest is roughly $533 during the draw period. The new property mostly covers its own costs, and you’ve used leverage to grow wealth. The risk? If either property sits vacant or needs major repairs, you’re on the hook for multiple mortgage payments plus the HELOC.

Common Mistakes Beginners Make

Overborrowing

The biggest mistake is maxing out the credit line just because it’s available. Yes, you might qualify for $100,000, but that doesn’t mean you should take it all. Many beginners borrow heavily for speculative projects or non-essential upgrades, then struggle when rental income dips or unexpected expenses hit. A safer approach is borrowing only what you need for projects with clear return-on-investment potential, like renovations that directly increase rent or property value.

Ignoring Variable Rates

Most investment property HELOCs have variable interest rates tied to the prime rate. When the Federal Reserve raises rates, your monthly payment goes up. I’ve seen investors lock in what seemed like a manageable 7% rate, only to watch it climb to 9.5% or 10% within two years. That can add hundreds of dollars to your monthly payment. Always stress-test your budget assuming rates could rise 2-3 percentage points. If you can’t afford payments at higher rates, you’re overleveraged.

Not Accounting for Rental Income Fluctuations

Beginner investors often assume rental income will remain constant. Reality is messier. Tenants leave, properties sit vacant, major repairs drain cash reserves, local markets soften. If your budget depends on 100% occupancy and steady rent, you’re setting yourself up for trouble. Experienced investors build in vacancy buffers—typically assuming 8-10% vacancy rates annually—and maintain cash reserves to cover at least six months of expenses including HELOC payments.

Practical Tips to Use Investment Property Equity Line of Credit Safely

Best Practices

First, only borrow for investments that generate measurable returns. Renovations should increase property value or rental income enough to justify the cost and interest. Buying additional properties should pencil out with realistic cash flow projections. Avoid using a HELOC for personal expenses or speculative ventures unrelated to your investment strategy.

Second, maintain healthy cash reserves separate from your credit line. Many investors mistakenly view their HELOC as an emergency fund. That’s dangerous because you’re paying interest on borrowed money, and if property values drop, your credit line could get frozen or reduced.

Third, make principal payments during the draw period if possible, even though they’re not required. This reduces your balance and the interest you’ll pay long-term. Treating it like interest-only free money for 10 years leads to payment shock later.

Risk Management

Lock in fixed-rate options if your lender offers them, even at a slightly higher rate, especially if you’re risk-averse or rates are rising. Monitor your debt-to-income ratio carefully—lenders may reduce or freeze your credit line if your financial situation deteriorates.

Consider the worst-case scenario: property values decline, rental income drops, and interest rates spike simultaneously. Could you still make payments? If not, you’re overextended. Scale back borrowing or improve cash flow before tapping equity aggressively.

Finally, work with a tax advisor to understand deductibility. Interest on HELOCs used for investment property improvements is generally tax-deductible, but rules are specific. Using HELOC funds for personal expenses typically isn’t deductible even if secured by investment property.

Frequently Asked Questions

Q1. What is the equity line of credit on an investment property?

It’s a revolving credit line secured by equity in a rental or investment property. You can borrow, repay, and borrow again during the draw period, paying interest only on what you use. It works like a HELOC on a primary residence but with stricter terms and higher rates.

Q2. Can you get a line of credit on investment property?

Yes, but it’s harder than getting one on your primary home. Lenders view investment properties as higher risk, so expect tougher credit requirements, larger down payments (or equity), higher interest rates, and more documentation proving rental income and financial stability.

Q3. What are typical rates and costs?

As of early 2025, rates for investment property HELOCs generally range from 8% to 11%, depending on your credit, equity, and lender. That’s typically 1-2 percentage points higher than primary residence HELOCs. Closing costs run 2-5% of the credit line and may include appraisal fees ($400-$600), origination fees (1-2% of the line), title insurance, and recording fees.

Q4. How much equity do I need?

Most lenders require at least 20-25% equity remaining after the HELOC is issued. With typical 75% LTV limits, you effectively need about 25% equity to access funds. Some lenders allow 80% LTV if you have excellent credit and strong cash flow, but that’s less common.

Q5. Who are the major lenders offering HELOCs on investment properties?

Not all banks offer investment property HELOCs. Figure, Third Federal Savings & Loan, and some regional banks and credit unions provide them. Bigger banks like Wells Fargo and Bank of America often don’t, or have very limited programs. You may also find options through online lenders, but shop carefully and compare terms. Rates, fees, and requirements vary significantly.

Q6. What happens if I can’t make payments?

The lender can foreclose on your investment property since it’s collateral for the HELOC. This is true even if your primary mortgage is current. Defaulting damages your credit severely and you lose the property. Unlike credit card debt, this isn’t unsecured—the consequences are serious and immediate.

Q7. Is the interest tax-deductible?

Generally yes, if you use the funds to buy, build, or substantially improve the investment property securing the loan. The IRS allows deductions for investment property mortgage interest as a business expense. However, if you use HELOC funds for personal expenses or unrelated investments, that interest typically isn’t deductible. Consult a tax professional for your specific situation.

Conclusion

An investment property equity line of credit can be a powerful tool for experienced real estate investors who need flexible access to capital for renovations, acquisitions, or strategic improvements. It lets you unlock equity without selling, offers revolving access to funds, and can genuinely accelerate portfolio growth when used intelligently. But it’s not free money, and it’s definitely not for everyone. The variable rates, stricter qualification requirements, higher costs, and foreclosure risk mean this approach demands discipline, solid cash reserves, and realistic financial projections. If you understand leverage, maintain healthy margins, and borrow strategically for projects with clear returns, it can work well. If you’re stretching to qualify, counting on perfect conditions, or using it to cover operating shortfalls, you’re playing with fire. Take time to model different scenarios, stress-test your budget, and honestly assess whether the additional debt enhances or endangers your investment strategy.

Word Count: ~2,000 words

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Consult with qualified financial and tax professionals before making investment decisions.