Introduction

Running a small investment firm — even a modest one managing a few million dollars — involves a surprising amount of financial recordkeeping. Transactions need to be tracked. Investor reports need to go out on time. Portfolio positions have to reconcile with custodian statements. And somewhere in all of that, you still need to meet compliance standards.

Many small firms discover too late that standard bookkeeping tools — the kind built for retail shops or freelancers — just don’t handle investment operations well. That’s where accounting software for investment company becomes relevant. Not as a luxury item, but as a practical operational necessity.

This article explains what this type of software actually does, how it works in a real investment context, what it costs, and what mistakes firms commonly make when choosing one. By the end, you’ll have a clearer picture of whether your firm actually needs a specialized system — and what to look for if it does.

What Accounting Software for Investment Company Really Means in Practice

The term gets used loosely, so it helps to be specific. Accounting software for investment company refers to systems built specifically to handle the financial operations of entities that manage assets on behalf of investors — whether that’s a registered investment advisor (RIA), a small hedge fund, a family office, or a private equity firm.

Standard accounting software like QuickBooks or Wave handles income, expenses, invoices, and payroll reasonably well. But investment operations involve a different layer of complexity: securities transactions, unrealized gains, performance reporting, capital account allocations, and regulatory filings that standard systems were never designed to support.

A proper investment accounting system — also called portfolio accounting software or fund accounting software — handles things like tracking individual portfolio positions and their cost basis, calculating realized and unrealized gains and losses, managing investor capital accounts for fund structures, producing performance reports for investors and compliance, reconciling transactions with prime brokers and custodians, and supporting SEC or IRS reporting requirements.

For a firm managing even $5–10 million in assets, doing this manually in spreadsheets is not just inconvenient — it’s a significant source of operational risk.

Quick Definition: Accounting software for investment companies manages securities transactions, portfolio positions, capital account allocations, and compliance reporting — tasks that general-purpose bookkeeping tools cannot handle effectively.

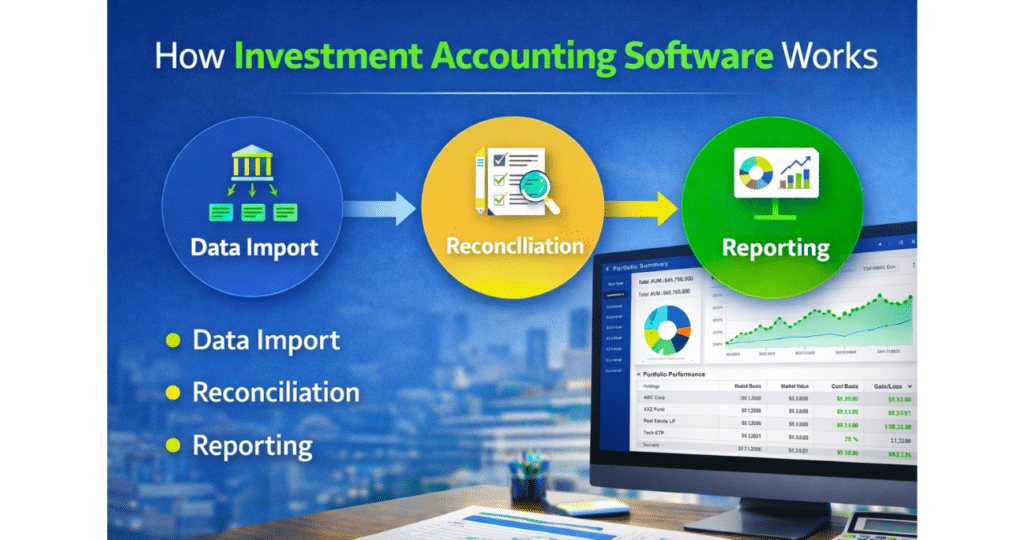

How Accounting Software for Investment Company Works Step by Step

It’s easier to understand when you walk through a real workflow. Suppose a small RIA manages separate accounts for 12 clients, with a total of $18 million in assets under management (AUM).

Step 1: Data Import and Transaction Capture

The system connects to custodians — Schwab, Fidelity, Pershing, or wherever client assets are held — and imports transaction data daily or in real time. This includes buys, sells, dividends, interest, corporate actions like splits or mergers, and cash movements. Manual entry is possible, but automation reduces errors significantly.

Step 2: Position Reconciliation

Once transactions are imported, the software compares its internal records against custodian statements. Any discrepancy — a missed dividend, a mismatched price, a delayed settlement — gets flagged. Reconciliation is one of the most time-consuming tasks in investment operations, and this is where firms using spreadsheets tend to struggle most.

Step 3: Performance and Gain/Loss Calculation

The system calculates portfolio returns — typically time-weighted returns (TWR) for comparison against benchmarks, and dollar-weighted returns (IRR) for actual investor experience. It also tracks each lot’s cost basis using FIFO, average cost, or specific identification, which matters for tax reporting.

Step 4: Investor Reporting

Monthly or quarterly, the system generates investor statements. For a fund structure, this includes capital account balances, profit and loss allocations, management fees charged, and performance net of fees. For separately managed accounts, it’s typically a portfolio summary and transaction history.

Step 5: Compliance and Audit Support

For SEC-registered firms, the software helps maintain the books and records required under the Investment Advisers Act of 1940. During audits — especially GIPS-compliant performance audits — having clean, traceable records is essential. Firms without proper systems often spend considerable time reconstructing data when auditors request documentation.

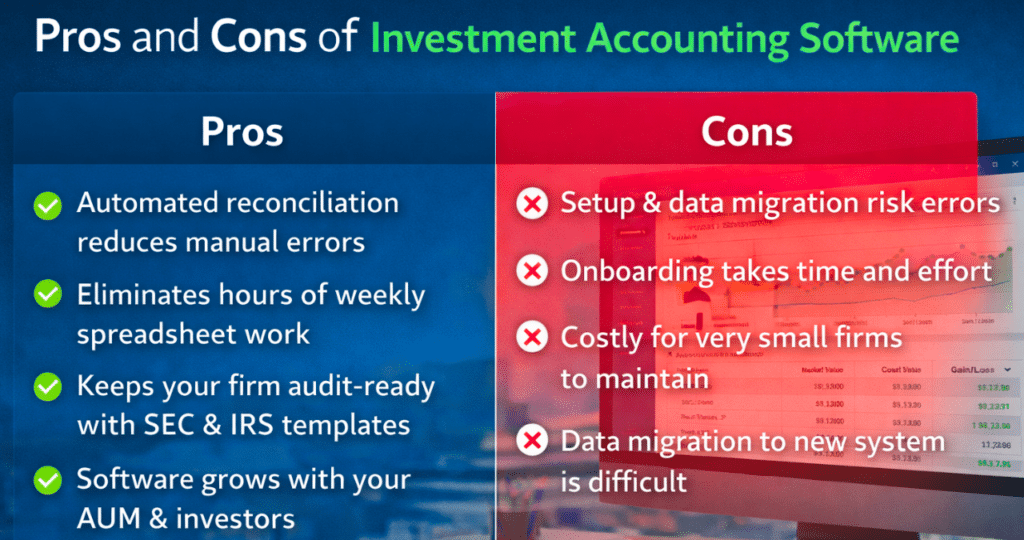

Pros and Cons of Accounting Software for Investment Company

Pros:

Automated reconciliation reduces manual errors significantly. The system eliminates hours of weekly spreadsheet work. Built-in SEC and IRS reporting templates keep your firm audit-ready. The software grows with your AUM and number of investors. Professional investor reports are generated automatically without starting from scratch every quarter.

Cons:

Setup and data migration can introduce errors if not done carefully. Initial onboarding takes time — weeks to months for complex portfolios. Compliance features vary widely, and not all systems meet every requirement. Enterprise systems priced at $500 to $2,000 or more per month are expensive for very small firms. Migrating data to a new system later is painful and costly. Some integrations require additional setup fees or IT support.

A Realistic Example Using Simple Numbers

Consider a small private equity firm — call it Clearfield Capital — that manages two funds with combined AUM of $22 million and 15 limited partners.

Before adopting investment accounting software, the firm used Excel for capital account tracking and a separate general ledger for fund expenses. Every quarter, producing LP statements took two staff members about three days each. Reconciling capital calls and distributions was done manually, often with errors that required correction calls to investors.

After moving to a dedicated fund accounting software solution, quarterly LP statements dropped from roughly six staff-days to about one day of review. Capital account reconciliation errors fell to near zero. Year-end K-1 preparation time for IRS partnership tax filing dropped by roughly 40%. The software cost approximately $1,200 per month — paid back in recovered staff time within the first quarter.

This isn’t a guarantee that the same results happen for every firm. Software implementation varies. But the pattern holds for many small investment operations that transition away from manual systems.

For contrast, a solo RIA managing $5 million in assets across 8 separately managed accounts might not need enterprise-level software. A mid-tier portfolio management system at $150 to $300 per month — or even a CRM with portfolio tracking built in — may be sufficient.

Common Mistakes Investment Firms Make When Choosing Accounting Software

Choosing a General Accounting Tool Instead of an Investment-Specific System

This is the most common mistake. QuickBooks and similar platforms are excellent for operating businesses. They aren’t built for securities accounting, capital allocations, or performance reporting. Firms that try to adapt them end up building complex workarounds that break down at scale.

Underestimating Reconciliation Complexity

Many firms don’t realize how much reconciliation work their team does until they start tracking it. Custodians have different data formats. Corporate actions are often misbooked. A system that automates reconciliation and flags exceptions is far more valuable than its price suggests. Not all software handles this equally well.

Buying Enterprise Software Before They’re Ready

Some small firms get sold on sophisticated platforms designed for $500M or larger institutions. The result is overpaying for features they won’t use for years, while spending weeks in implementation. A $22M AUM firm doesn’t need the same system as a $2 billion fund. Matching software to actual operational complexity matters.

Ignoring SEC Compliance Requirements

Registered investment advisors in the U.S. must maintain specific books and records under Rule 204-2 of the Investment Advisers Act. Not all accounting software supports this out of the box. Firms that discover this gap during an SEC examination face significant operational disruption.

Not Evaluating Data Migration Costs

Switching software after two or three years is painful. Historical transaction data, cost basis records, and investor documents need to transfer cleanly. Firms that don’t evaluate migration complexity — or vendor support for migration — often end up paying consultants to manually reconstruct records.

Practical Tips to Choose the Right Accounting Software for Your Investment Company

Know Your AUM Range and Firm Type

Software that works well for a $10M RIA with individual client accounts is different from what a $50M private equity fund needs. Private equity and hedge fund structures require proper fund accounting with capital call tracking, waterfall calculations, and LP reporting. RIAs managing separate accounts need portfolio performance tools and client-facing reporting.

Verify Custodian Connectivity

Before committing to any system, confirm it connects directly to your custodians via data feeds. Manual data entry is a liability. Ask specifically which custodians are supported and how frequently data syncs.

Ask About SEC Rule 204-2 Compliance

If you’re an SEC-registered advisor, your software needs to support compliant books and records retention. Ask vendors directly which regulatory requirements their platform was built to meet, and get it in writing if possible.

Request a Trial Period or Pilot

Most reputable investment accounting vendors will allow a trial or proof-of-concept period. Use actual firm data with appropriate protections to see how reconciliation handles your custodians’ real feeds. Don’t evaluate software in isolation from your actual data.

Think About Who Will Use It

Some platforms assume you have a dedicated operations person or a fund administrator. Others are designed to be used by a solo practitioner with limited accounting background. The usability gap between systems is significant. Software that requires constant consultant support to operate is not sustainable for small teams.

Consider Total Cost of Ownership

Licensing fees are one part of cost. Implementation, training, data migration, ongoing support, and potential consultant fees are the rest. A system priced at $800 per month can easily cost $20,000 to $40,000 in year one when implementation is factored in. Plan for that honestly before signing contracts.

Frequently Asked Questions

Q1: Can a small investment firm just use QuickBooks for fund accounting?

For very basic operating expenses — office rent, payroll, vendor invoices — QuickBooks works fine. But it doesn’t handle securities transactions, portfolio positions, capital account allocations, or investor-level reporting. Most firms that try to run fund accounting in QuickBooks eventually hit a wall and spend significant time on workarounds. If you manage external investor capital, a specialized system is worth evaluating early.

Q2: What does investment accounting software typically cost?

It varies widely. Entry-level portfolio tracking tools designed for small RIAs can run $100 to $400 per month. Mid-tier platforms for firms with $10M to $100M AUM typically range from $500 to $1,500 per month. Enterprise systems for larger funds or complex structures can exceed $2,000 to $5,000 per month depending on transaction volume and number of funds. Implementation costs are usually separate.

Q3: What is fund accounting, and is it different from regular accounting?

Yes, meaningfully different. Fund accounting tracks the financial activity of an investment fund as a whole, as well as each investor’s proportional share — called a capital account. It handles income allocation, management fee calculations, carried interest for private equity, and distributions. General accounting software handles income statements and balance sheets but wasn’t built for this layer of complexity.

Q4: Does my software need to comply with SEC requirements?

If you’re registered with the SEC as an investment adviser, yes. Rule 204-2 requires you to maintain specific books and records — including trade records, client account records, and performance documentation — for defined retention periods. The software you use needs to support this, or you’ll need to maintain compliant records separately. This is worth verifying with your compliance consultant before selecting a platform.

Q5: What is portfolio reconciliation and why does it matter?

Reconciliation is the process of comparing your internal records against what your custodian or prime broker shows. If your system says a client holds 500 shares of a stock but the custodian shows 480, there’s a discrepancy that needs to be resolved. These differences happen more often than people expect — from timing differences, corporate actions, or data errors. Unreconciled positions create reporting errors and compliance risk. Good software automates this comparison and flags exceptions for review.

Q6: Can I integrate accounting software with a CRM system?

Many modern investment accounting platforms offer CRM integration — connecting client data, communication history, and account details across systems. Whether this matters depends on your firm’s size and workflow. For RIAs with active client relationships, a unified view of client accounts and communication history can save time. For fund managers dealing with a smaller number of institutional LPs, CRM integration may be less critical than reporting and reconciliation capabilities.

Q7: When should a small firm hire a fund administrator instead of using software directly?

Fund administrators are third-party firms that handle accounting, investor reporting, and back-office operations on your behalf. For very early-stage funds, outsourcing to a fund administrator may be more cost-effective than building internal systems. As AUM grows and the fund matures, bringing accounting in-house with dedicated software often makes financial sense. There’s no fixed AUM threshold — it depends on fee income, staff capacity, and LP expectations around reporting quality.

Final Thoughts

Accounting software for investment companies isn’t a complicated concept — it’s specialized tooling for an industry that has genuinely specialized needs. The firms that struggle most are usually the ones that either delay building proper systems until operational problems force their hand, or jump to enterprise platforms without evaluating whether the complexity matches their actual size.

If you’re managing external capital — even a modest amount — it’s worth taking time to map out your actual operational workflow before choosing a system. Know what your custodians support. Understand your compliance obligations. And talk to other firms at a similar stage who’ve gone through the selection process.

The right software won’t transform your investment strategy. But it will free up time, reduce errors, and make your operation more defensible when regulators or investors ask questions. That’s a reasonable thing to aim for.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investment decisions should be made in consultation with a qualified financial professional. SEC compliance requirements may vary based on your firm’s registration status and assets under management.