Investing in stocks feels overwhelming when you’re just starting out. You see conflicting advice everywhere—some people say buy individual stocks, others recommend index funds, and everyone seems to have a different opinion about timing the market. If you’ve been searching for a straightforward approach that doesn’t require you to become a financial expert overnight, you’ve probably come across the pedro vaz paulo stocks investment methodology. This approach focuses on building wealth through careful stock selection, diversification, and patience rather than chasing quick profits.

This matters because most beginners lose money not from picking bad stocks, but from making emotional decisions and lacking a clear strategy. By the end of this article, you’ll understand how this investment philosophy works, what it requires from you, and whether it matches your financial situation and temperament.

What Pedro Vaz Paulo Stocks Investment Really Means in Everyday Investing

The pedro vaz paulo stocks investment approach centers on fundamental analysis and long-term value creation. Instead of jumping on trending stocks or following social media hype, this methodology emphasizes researching companies with solid financials, competitive advantages, and sustainable business models.

For ordinary investors, this means spending time understanding what you’re buying. You’re not gambling on price movements—you’re becoming a partial owner of real businesses. The philosophy rejects day trading and market timing in favor of holding quality stocks through market cycles.

What makes this different from other strategies? It acknowledges that most people have jobs and lives outside of investing. You don’t need to watch stock tickers all day. The focus stays on selecting good companies at reasonable prices and letting compound growth do the heavy lifting over decades.

This approach suits people who can commit to learning basic financial concepts but don’t want investing to become a second career. It’s honest about requiring patience—your money won’t double overnight, but it has a better chance of growing steadily over 20 or 30 years.

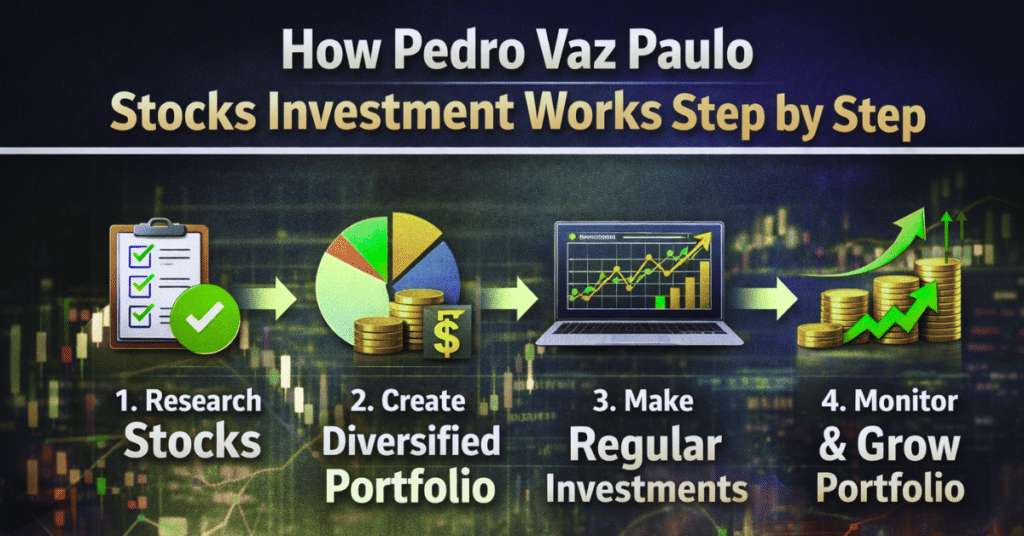

How Pedro Vaz Paulo Stocks Investment Works Step by Step (Real-Life Flow)

Portfolio Building Foundation

You start by identifying 15 to 25 quality stocks across different sectors. This isn’t random selection. You’re looking at companies with consistent revenue growth, manageable debt levels, and products or services people will need in five or ten years.

The research phase takes work. You’ll read annual reports, compare financial ratios, and understand what each company actually does. Many beginners skip this step and regret it later when their hastily chosen stocks drop 30% and they panic sell.

Diversification Strategy

Spreading investments across healthcare, technology, consumer goods, utilities, and financial sectors protects you when one industry struggles. If your tech stocks drop during a sector correction, your utility and consumer staple holdings might stay stable or even gain value.

Real diversification means more than just buying different stock tickers. It means understanding that your portfolio shouldn’t collapse if one sector hits trouble. A realistic split might be 20% technology, 20% healthcare, 15% financials, 15% consumer staples, 15% industrials, and 15% in other sectors.

Long-Term Perspective

This methodology assumes you’re investing for at least 10 years, ideally 20 to 30. Short-term volatility doesn’t matter much when you’re building wealth for retirement or major life goals decades away.

During market downturns—and they will happen—you don’t sell in panic. In fact, market drops often present buying opportunities if you have cash available and your chosen companies’ fundamentals haven’t changed.

Risk Management Techniques

Position sizing matters more than most beginners realize. No single stock should represent more than 5% to 8% of your total portfolio when you’re starting out. This prevents one bad pick from destroying your savings.

You also maintain an emergency fund outside your stock portfolio. The standard recommendation is three to six months of living expenses in a high-yield savings account. This keeps you from selling stocks at the worst possible time just to cover unexpected expenses.

Pros and Cons of Pedro Vaz Paulo Stocks Investment (Honest, Balanced Table)

| Realistic Benefits | Honest Trade-offs |

|---|---|

| Builds genuine wealth over decades through compound growth | Requires 10+ years to see meaningful results; not suitable for short-term goals |

| Lower stress than day trading or constant portfolio adjustments | Demands upfront learning about financial statements and business analysis |

| Historically outperforms savings accounts and bonds over long periods | Market downturns of 20-40% will test your emotional discipline |

| Creates potential passive income through dividend-paying stocks | No guarantees; even quality companies can fail or underperform |

| Provides hedge against inflation as stock values typically rise over time | Requires consistent contributions; one-time investments grow slower |

| Tax advantages for long-term holdings (lower capital gains rates) | Opportunity cost if you need money locked in stocks for emergencies |

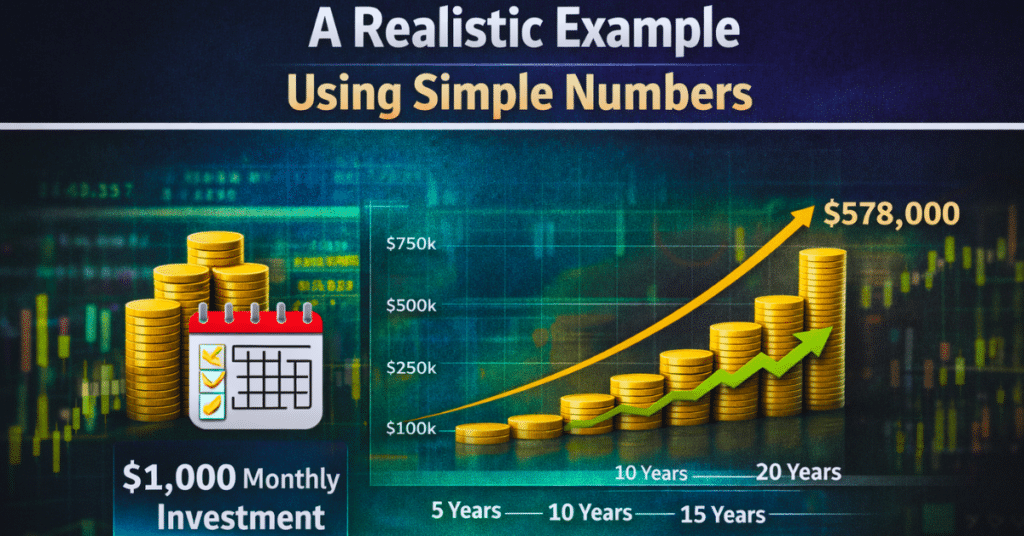

A Realistic Example Using Simple Numbers

Let’s say you’re 35 years old and can invest $1,000 monthly into a diversified stock portfolio following this methodology.

Year 1-5: Your contributions total $60,000. With average annual returns around 7% after inflation (a reasonable historical expectation, not a guarantee), your portfolio might grow to approximately $71,500. Not dramatic, but you’re building the foundation.

Year 6-15: You’ve now contributed $180,000 total. With continued 7% average returns, your portfolio could reach roughly $260,000. Compound growth accelerates—your earlier investments have had more time to grow.

Year 16-30: Your total contributions reach $360,000. With the same average return, your portfolio might grow to approximately $1.13 million. Notice that your actual contributions were $360,000, but compound growth added over $770,000.

Important Reality Check: These numbers assume you never panic-sell during downturns, maintain consistent monthly investments even when markets drop, and achieve historical average returns. Many investors fail at one or more of these requirements.

Some years will return 15% or 20%. Others will lose 10% or more. The 7% figure represents a long-term average that smooths out the volatility. Your actual experience will feel much bumpier.

Common Mistakes Beginners Make

Over-Trading and Constant Adjustments

New investors check their portfolios daily and make changes based on short-term price movements. This generates unnecessary transaction costs and often means selling winners too early while holding losers too long.

The data shows that investors who trade frequently typically underperform those who buy quality stocks and hold them. Transaction fees, taxes on short-term gains, and poor timing decisions all eat into returns.

Chasing Trends and Hot Stocks

When everyone talks about a particular stock or sector, beginners assume they’re missing out. They buy high after major price increases, then watch their investment drop when the hype fades.

Cannabis stocks in 2018, meme stocks in 2021—the pattern repeats. By the time ordinary investors hear about the trend, early investors are often taking profits.

Ignoring Diversification

Putting too much money into one stock or sector feels fine when it’s rising. Then a single company scandal, regulatory change, or earnings miss can wipe out years of gains overnight.

Diversification feels boring compared to betting everything on your highest-conviction idea. But it’s the difference between recovering from mistakes and experiencing financial disaster.

Emotional Decision-Making

Fear and greed drive more investment losses than poor stock selection. Selling everything during a market crash locks in losses. Buying with borrowed money during euphoric highs leads to devastating losses when corrections arrive.

Successful investing requires separating your emotions from your strategy. Having a written investment plan helps, but following it when your account balance drops 25% tests everyone’s discipline.

Practical Tips to Use Pedro Vaz Paulo Stocks Investment Safely

Start with Education Before Money

Spend one to three months learning basic concepts before investing real money. Understand terms like P/E ratio, revenue growth, profit margins, and cash flow. Free resources from Investopedia and Khan Academy cover these fundamentals well.

Open a brokerage account but start with small amounts while you’re learning. Losing $500 on a mistake teaches valuable lessons. Losing $50,000 might end your investing journey permanently.

Build Your Portfolio Gradually

Don’t invest your entire savings at once, even if you’re confident. Dollar-cost averaging—investing fixed amounts regularly—reduces the risk of buying everything right before a market crash.

Add new positions over six to twelve months. This gives you time to research each company properly and spreads your entry points across different market conditions.

Create Clear Investment Criteria

Write down what qualifies as a good investment for your portfolio. This might include minimum market capitalization, debt-to-equity ratios, revenue growth rates, and dividend history.

When you’re tempted by a stock that doesn’t meet your criteria, your written rules keep you disciplined. Without these guidelines, every stock looks attractive for some reason.

Track Performance Honestly

Review your portfolio quarterly, not daily. Compare your returns to relevant benchmarks like the S&P 500. If you’re consistently underperforming index funds, you should question whether individual stock picking makes sense for you.

Many investors lie to themselves about performance, ignoring fees and taxes or cherry-picking their best picks while forgetting their losers. Honest tracking reveals whether your strategy actually works.

Maintain Appropriate Position Sizes

As mentioned earlier, individual stocks shouldn’t exceed 5% to 8% of your portfolio initially. As you gain experience and your portfolio grows, you might adjust this, but conservative position sizing protects beginners from catastrophic losses.

If one stock performs exceptionally well and grows to 15% or 20% of your portfolio, consider trimming it back. This feels counterintuitive—why sell your winners?—but it maintains your risk management discipline.

Frequently Asked Questions

Q1. Which is the best stock to invest now?

There’s no universal “best stock” that works for everyone at all times. The right stocks for you depend on your risk tolerance, investment timeline, and portfolio needs. Quality companies with competitive advantages, solid financials, and reasonable valuations deserve research, but what’s “best” changes based on market conditions and your specific situation.

Q2. How much monthly investment is needed for passive income?

This depends entirely on your income goals and expected returns. If you want $1,000 monthly passive income from dividend stocks yielding 4%, you’d need a portfolio worth $300,000. Building this through monthly investments of $1,000 would take roughly 18-20 years assuming 7% average annual returns. Smaller monthly contributions extend this timeline significantly.

Q3. What is the 7% rule in stock investing?

The 7% rule refers to the approximate average annual return of the stock market after adjusting for inflation over very long periods (50+ years). It’s not a guarantee or a law—just a historical observation. Some decades return much more, others much less. Investors use this figure for retirement planning, understanding it represents an average smoothing out major volatility.

Q4. Can stocks create reliable retirement income?

Stocks can contribute to retirement income through dividends and strategic selling, but “reliable” requires qualification. Dividend-paying stocks from established companies provide more predictable income than growth stocks, but even dividends can be cut during economic downturns. Most financial advisors recommend diversifying retirement income across stocks, bonds, and other assets rather than relying solely on stock portfolios.

Q5. How much should I invest to earn $1,000/month?

For dividend income, you’d need roughly $300,000 to $400,000 invested in stocks yielding 3% to 4% annually. Building this amount requires consistent investing over many years. If you invest $1,000 monthly with 7% average annual returns, reaching $300,000 takes approximately 18 years. Higher monthly contributions shorten this timeline; lower contributions extend it significantly.

Q6. Is this approach suitable for everyone?

No investment strategy suits everyone. This methodology works best for people with stable income, 10+ year time horizons, emotional discipline during market downturns, and willingness to learn basic financial analysis. It doesn’t suit people needing money within five years, those uncomfortable with temporary losses of 20-40%, or individuals preferring completely hands-off investing (who might prefer target-date funds or robo-advisors).

Q7. What happens during market crashes?

Your portfolio value will drop, sometimes dramatically. During the 2008 financial crisis, the S&P 500 fell about 57% from peak to bottom. The COVID-19 crash in March 2020 saw drops of 34% in just weeks. The strategy requires continuing your contributions during these periods and not selling. Historically, markets recover, but the timeline varies—sometimes months, sometimes years.

Conclusion

The pedro vaz paulo stocks investment approach offers a realistic path to building wealth through stocks, but it demands patience, education, and emotional discipline. You won’t get rich quickly, and you’ll face periods where your account balance drops significantly. These are features of stock investing, not bugs.

Understanding that successful investing means buying quality companies and holding through volatility gives you a framework for making decisions. It won’t eliminate the anxiety of watching your savings fluctuate, but it provides reasoning to counter panic during downturns.

If you’re considering this approach, start small, educate yourself thoroughly, and be honest about whether you can maintain discipline during inevitable market crashes. There’s no shame in deciding that index funds or professionally managed portfolios better match your personality and circumstances.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Consult with a qualified financial advisor before making investment decisions.