Introduction

Building a strong financial future is like constructing a house—you need a solid foundation. In personal finance, experts have identified five key foundations that help you manage money wisely and achieve long-term security.

The second foundation in personal finance is all about living on less than you make. This means spending less money than you earn and creating a budget that works for your lifestyle.

Before we dive deep into the second foundation, let’s understand what these foundations are and why they matter. The first foundation focuses on saving an emergency fund, the second teaches budgeting and expense control, and the third deals with managing debt. Each step builds on the previous one, creating a roadmap to financial freedom.

In this guide, we’ll explore everything about the second foundation—what it means, why it matters, and how you can apply it to your own life starting today.

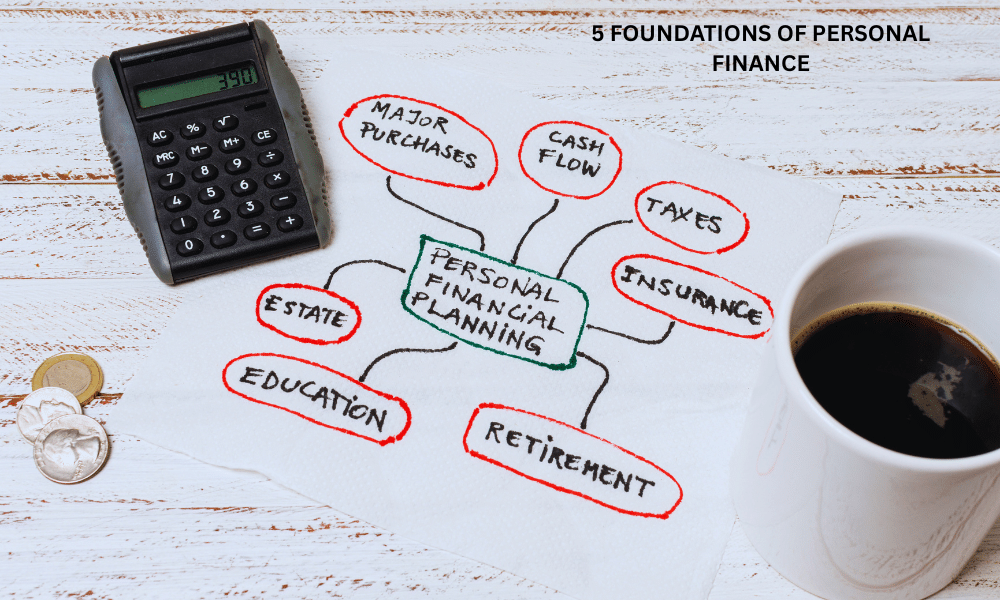

What Are the Foundations of Personal Finance?

The foundations of personal finance are basic principles that guide your money decisions. Think of them as building blocks that support your entire financial life.

These foundations help you avoid common money mistakes. They teach you how to save, spend wisely, stay out of debt, and plan for the future.

Why do foundations matter? Without a strong base, your financial plans can collapse easily. Just like a house needs a solid foundation to stand strong, your finances need structure and discipline.

Financial experts like Dave Ramsey have popularized these foundations through educational programs. They’re designed specifically for students and beginners who want to take control of their money.

What Are the 5 Foundations of Personal Finance in Order?

Let’s break down all five foundations so you understand where the second foundation fits in the bigger picture.

First Foundation: Build an Emergency Fund

The first foundation in personal finance focuses on saving $500 to $1,000 for emergencies. This money acts as a safety net when unexpected expenses pop up.

Think of emergency funds as your financial cushion. If your car breaks down or you have a medical bill, you won’t need to use credit cards or borrow money.

Starting small makes this goal achievable. Even saving $50 per month gets you there within 10 to 20 months.

Second Foundation: Living on Less Than You Earn

The second foundation of personal finance teaches you to spend less than you make. This means creating a budget, tracking expenses, and controlling your spending habits.

This foundation is about discipline and awareness. You need to know where every dollar goes each month.

Living below your means prevents debt and creates room for saving and investing. It’s the cornerstone of financial success.

Third Foundation: Manage and Pay Off Debt

The third foundation in personal finance focuses on eliminating debt using strategies like the debt snowball method. You start by paying off smallest debts first, then move to larger ones.

Debt keeps you stuck financially. The third foundation helps you break free and build wealth without monthly loan payments dragging you down.

Fourth Foundation: Invest for the Future

Once debt is gone, you start investing. This foundation focuses on retirement accounts, stocks, mutual funds, and building long-term wealth.

Investing early gives your money time to grow through compound interest.

Fifth Foundation: Give and Build Wealth

The final foundation emphasizes generosity and legacy building. When you’re financially secure, you can help others and leave a lasting impact.

This foundation reminds us that money isn’t just about personal gain—it’s also about making a difference.

What Is the Second Foundation of Personal Finance?

Now let’s focus on the star of this article: the second foundation in personal finance.

This foundation is simple but powerful: spend less than you earn. It means living within your means and creating a monthly budget that balances income and expenses.

Why does this matter? If you spend everything you make (or worse, spend more), you’ll never build savings or wealth. You’ll always feel financially stressed.

Key Elements of the Second Foundation

1. Budgeting: Creating a plan for your money before the month begins.

2. Tracking expenses: Knowing exactly where your money goes—every coffee, subscription, and grocery trip.

3. Controlling spending: Making conscious choices about needs versus wants.

4. Creating margin: Leaving room between income and expenses for saving and unexpected costs.

Real-Life Example

Let’s say Sarah earns $3,000 per month after taxes. If she spends $3,200, she goes into debt. But if she spends only $2,500, she has $500 left over for savings, investments, or emergencies.

That $500 difference changes everything. It’s the foundation of financial security.

What Is the Second Foundation in Personal Finance (Dave Ramsey)?

Dave Ramsey is a famous financial expert who teaches these foundations through his “Foundations in Personal Finance” curriculum used in schools nationwide.

According to Ramsey, the second foundation emphasizes budgeting as the foundation of all financial success. He often says, “A budget is telling your money where to go instead of wondering where it went.”

Ramsey teaches the zero-based budget method. This means assigning every dollar a job before the month starts. Income minus expenses should equal zero—meaning every dollar has a purpose.

Why does budgeting come before debt payoff and investing? Because without controlling spending, you’ll never have money left over to pay extra on debt or invest for retirement.

The second foundation creates financial breathing room. It’s the bridge between emergency savings (first foundation) and debt elimination (third foundation).

First Foundation vs Second Foundation in Personal Finance

Let’s compare these two foundations side by side:

| Aspect | First Foundation | Second Foundation |

|---|---|---|

| Focus | Saving for emergencies | Budgeting and spending control |

| Goal | $500–$1,000 emergency fund | Live on less than you make |

| Purpose | Financial safety net | Prevent debt and create margin |

| Timeframe | Short-term (save quickly) | Ongoing habit (every month) |

| Action | One-time savings goal | Continuous monthly practice |

| Result | Protection from surprises | Long-term financial stability |

Both foundations work together. The first gives you security, while the second ensures you don’t fall back into financial trouble.

Benefits of the Second Foundation in Personal Finance

Mastering the second foundation brings life-changing benefits. Here’s what happens when you consistently live below your means:

Financial Discipline and Self-Control

Budgeting teaches you to say “no” to impulse purchases. You learn delayed gratification—waiting for things instead of buying everything immediately.

This discipline spills over into other life areas. You become more intentional with decisions and less influenced by advertising or peer pressure.

Preventing Lifestyle Inflation

Lifestyle inflation means increasing your spending whenever your income rises. You get a raise, so you upgrade your car, apartment, and wardrobe.

The second foundation fights this trap. Instead of spending more when you earn more, you save and invest the difference.

Supporting Saving and Investing Goals

When you spend less than you earn, you create cash flow margin. This extra money funds your emergency fund, retirement accounts, and future goals.

Without the second foundation, you’ll never have money left over for wealth-building activities.

Common Mistakes People Make With the Second Foundation

Even with good intentions, people struggle with budgeting. Here are the biggest mistakes:

Not tracking expenses: You can’t manage what you don’t measure. Many people have no idea where their money actually goes each month.

Overspending on wants: Confusing needs (housing, food, transportation) with wants (streaming services, dining out, new clothes) destroys budgets.

Inconsistent budgeting: Creating a budget once isn’t enough. You need to review and adjust it monthly based on changing circumstances.

Ignoring small purchases: Those $5 coffees and $10 subscriptions add up to hundreds per month. Small leaks sink big ships.

No accountability: Going solo makes budgeting harder. Share your goals with a friend or partner for support.

How to Apply the Second Foundation Step by Step

Ready to master the second foundation? Follow these practical steps:

Step 1: Track Your Income

Write down all money coming in each month. Include your salary, side hustle income, freelance work, and any other sources.

Be accurate. Use after-tax income (take-home pay), not gross salary.

Step 2: Categorize Your Expenses

List every expense category: rent, utilities, groceries, transportation, insurance, entertainment, debt payments, and savings.

Review bank statements and credit card bills from the past three months to catch everything.

Step 3: Create a Monthly Budget

Assign a dollar amount to each category. Make sure total expenses are less than total income.

Use the 50/30/20 rule as a starting point: 50% needs, 30% wants, 20% savings and debt payoff.

Step 4: Review and Improve Monthly

At month’s end, compare actual spending to your budget. Where did you overspend? Where did you do well?

Adjust next month’s budget based on what you learned. Budgeting improves with practice.

Second Foundation in Personal Finance (Simple Budget Table)

Here’s a practical budget example for someone earning $3,000 monthly:

| Category | Budgeted Amount | Percentage |

|---|---|---|

| Rent/Housing | $900 | 30% |

| Groceries | $300 | 10% |

| Transportation | $250 | 8% |

| Utilities | $150 | 5% |

| Insurance | $200 | 7% |

| Entertainment | $200 | 7% |

| Dining Out | $150 | 5% |

| Savings | $450 | 15% |

| Debt Payment | $300 | 10% |

| Miscellaneous | $100 | 3% |

| Total | $3,000 | 100% |

Notice that expenses equal income, but there’s built-in savings. This person is living on less than they make by prioritizing savings first.

Who Should Focus on the Second Foundation?

The second foundation benefits everyone, but it’s especially critical for:

Students: Learning budgeting early prevents decades of financial mistakes. Start now, even with small amounts.

New earners: Your first job is the perfect time to build smart money habits. Don’t let lifestyle inflation steal your future.

Budgeting beginners: If you’ve never created a budget, start today. It’s never too late to take control of your finances.

Frequently Asked Questions (FAQs)

Q1. What is the second foundation in personal finance?

The second foundation is living on less than you make. It focuses on budgeting, controlling expenses, and spending less than your income to create financial margin.

Q2. What was the first foundation in personal finance?

The first foundation is saving a $500–$1,000 emergency fund. This provides a financial cushion for unexpected expenses before you focus on budgeting.

Q3. What is the third foundation of personal finance?

The third foundation is paying off debt using strategies like the debt snowball method. You eliminate debt systematically after mastering budgeting.

Q4. What are the 5 foundations of personal finance?

The five foundations are: (1) Emergency fund, (2) Living below your means, (3) Debt payoff, (4) Investing, and (5) Building wealth and giving.

Q5. What is the second foundation in personal finance Quizlet?

On Quizlet and educational platforms, the second foundation is defined as budgeting and living on less than you earn—controlling spending to avoid debt.

Q6. Why is the second foundation important?

It creates financial discipline, prevents debt, enables saving, and builds the foundation for investing and wealth-building. Without it, other foundations fail.

Key Takeaways of the Second Foundation

- Live below your means every single month without exception

- Create and maintain a monthly budget that tracks every dollar

- Distinguish between needs and wants to control unnecessary spending

- Build financial discipline through consistent budgeting habits

- Create cash flow margin for savings, investing, and future goals

- Prevent lifestyle inflation when your income increases

- Review your budget monthly and adjust based on actual spending

Conclusion – Why the Second Foundation in Personal Finance Matters

The second foundation in personal finance is the cornerstone of financial success. Living on less than you make isn’t just about budgeting—it’s about building a life of financial freedom and security.

This foundation prevents debt, reduces financial stress, and creates opportunities for saving and investing. It transforms your relationship with money from reactive to intentional.

Whether you’re a student just starting out or someone looking to take control of finances, mastering the second foundation changes everything. Start today by tracking your expenses and creating your first budget.

Remember: Financial freedom begins when you spend less than you earn. Make the second foundation your daily practice, and watch your financial future transform.

Your journey to financial independence starts with one simple decision—living below your means. Start now.