This article is for informational purposes only and does not constitute financial advice.

When you’re building a stable financial life, it helps to follow a clear sequence. The third foundation in personal finance is often described as saving for retirement or building wealth through long-term investing—but what does that actually mean for someone just starting out? This guide walks through the concept step by step, using real numbers, honest trade-offs, and practical examples that reflect how everyday people manage money.

Understanding the foundations of personal finance isn’t about following rigid rules. It’s about creating a structure that protects you from emergencies, helps you avoid debt traps, and gradually builds long-term security. The third foundation comes after you’ve handled the basics: saving an emergency fund and eliminating high-interest debt. Once those are in place, you’re ready to focus on wealth-building and retirement planning.

What the Third Foundation in Personal Finance Really Means in Everyday Life

The third foundation in personal finance refers to investing for long-term goals, primarily retirement. After you’ve saved an emergency fund (usually $500–$1,000 to start, then 3–6 months of expenses) and paid off high-interest debt like credit cards, the next logical step is putting money into accounts that grow over time through compound interest and market returns.

Why does this matter? Because savings accounts alone won’t build wealth. With average interest rates around 0.5%–5% annually (as of early 2025), inflation erodes purchasing power. Investing in retirement accounts like a 401(k) or IRA typically offers average annual returns of 7%–10% over decades, adjusted for inflation. This difference compounds dramatically over 20–40 years.

The third foundation isn’t about getting rich quickly. It’s about consistent, disciplined contributions that take advantage of tax-advantaged accounts and compound growth. For most people, this means contributing 10%–15% of gross income toward retirement, starting as early as possible.

According to Investopedia, the power of compounding means that someone who starts investing $300/month at age 25 could accumulate significantly more by age 65 than someone who starts at age 35, even if the later starter contributes more total dollars. Time is the most valuable asset in long-term financial planning.

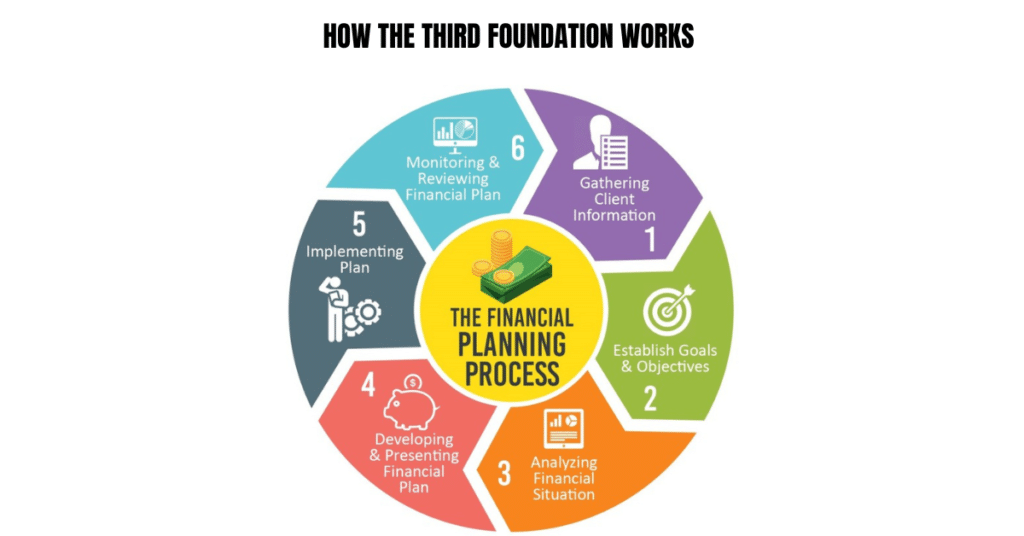

How the Third Foundation Works Step by Step (Real-Life Flow)

Let’s break down how this foundation works in practice:

Step 1: Confirm Your Foundation is Solid

Before investing for retirement, make sure you have $1,000–$2,000 in emergency savings and no credit card debt. If you’re still paying 18%–24% interest on cards, that takes priority. You can’t out-earn high-interest debt through investments.

Step 2: Choose the Right Account

Most Americans start with employer-sponsored 401(k) plans or individual Roth IRAs. A 401(k) often includes employer matching—free money that typically returns 50%–100% on contributions up to 3%–6% of salary. If your employer matches 50% of contributions up to 6% of your salary, and you earn $50,000 annually, contributing $3,000/year gets you an additional $1,500 from your employer.

Step 3: Start Small and Increase Gradually

You don’t need to invest 15% immediately. Start with enough to capture the full employer match (often 3%–6% of salary), then increase 1%–2% annually. Someone earning $45,000 might start by contributing $135/month (3%), then gradually reach $562/month (15%) over several years.

Step 4: Choose Low-Cost Index Funds

Most beginners benefit from target-date funds or broad index funds like those tracking the S&P 500. These diversify risk across hundreds or thousands of companies and charge minimal fees (0.03%–0.20% annually). Avoid individual stock picking unless you have expertise and time.

Step 5: Automate and Ignore Short-Term Volatility

Set up automatic contributions from each paycheck. Markets fluctuate—sometimes dramatically—but long-term investors benefit from dollar-cost averaging, buying more shares when prices are low and fewer when prices are high. Over 20–30 years, this smooths out volatility.

Here’s how it connects to earlier foundations: The first foundation (emergency savings) prevents you from withdrawing retirement funds during emergencies. The second foundation (debt elimination) ensures you’re not losing more to interest than you’re gaining from investments. The third foundation builds on that stability by creating long-term growth.

Pros and Cons of the Third Foundation (Honest, Balanced Table)

| Benefits | Limitations |

|---|---|

| Compound growth: $300/month invested at 8% annual return grows to approximately $440,000 in 30 years | Long time horizon: Money is typically locked until age 59½ without penalties |

| Tax advantages: Traditional 401(k) contributions reduce current taxable income; Roth contributions grow tax-free | Market risk: Investments can lose value in downturns (e.g., 2008, 2020) |

| Employer matching: Free money that instantly boosts returns by 50%–100% on matched amounts | Requires discipline: Easy to stop contributions during tight months |

| Inflation protection: Historical stock returns (7%–10%) outpace inflation (2%–3%) over decades | Fees matter: High expense ratios (1%+) can reduce returns by hundreds of thousands over time |

| Automatic contributions: Builds wealth without active decision-making each month | Complexity: Choosing between Roth vs. traditional, funds, and contribution limits can feel overwhelming |

The biggest advantage beginners overlook is employer matching—it’s an immediate 50%–100% return that no other investment guarantees. The biggest limitation is liquidity: retirement funds aren’t easily accessible for emergencies, which is why the emergency fund comes first.

A Realistic Example Using Simple Numbers

Meet Sarah, age 28, earning $52,000 annually as a marketing coordinator. She’s completed the first two foundations: $3,000 emergency fund and zero credit card debt. Now she’s ready for the third foundation.

Her Plan:

Sarah’s employer offers a 401(k) with a 50% match on contributions up to 6% of salary. She decides to start by contributing 6% ($260/month) to capture the full match. Her employer adds $130/month, so her account receives $390/month total.

Year 1 Results:

- Sarah contributes: $3,120

- Employer match: $1,560

- Total invested: $4,680

- Assuming 8% average annual return: balance after one year is approximately $4,867

5-Year Projection:

If Sarah maintains $390/month contributions (her $260 + employer’s $130) with 8% annual returns:

- Total contributions: $23,400

- Estimated account value: $28,900

- Growth from returns: $5,500

After 5 years, Sarah also increases her contribution to 10% of salary ($433/month), plus the employer match ($130), totaling $563/month. By age 65, continuing this pattern, her account could reach $800,000–$1,000,000, assuming historical market returns.

This example shows why starting early matters. Even modest contributions grow substantially over decades through compound interest and market appreciation.

Common Mistakes Beginners Make

1. Waiting to Start Until Finances Feel “Perfect”

Many people delay investing until they earn more or feel more secure. But someone who starts investing $200/month at age 25 accumulates far more than someone who waits until 35 and invests $400/month, even though the second person contributes more total dollars. Time compounds wealth more than amount.

2. Not Capturing the Full Employer Match

Failing to contribute enough to get the full employer match is leaving free money on the table. If your employer matches 50% of contributions up to 6% of salary, contributing only 3% means you’re forfeiting half the available match.

3. Ignoring Fees and Expense Ratios

A fund charging 1% annually versus 0.10% might seem minor, but over 30 years, that 0.9% difference can cost $100,000+ on a $500,000 portfolio. Always choose low-cost index funds when possible.

4. Panicking During Market Downturns

Selling investments when the market drops 20%–30% locks in losses. Historical data shows markets recover over time. The 2008 crash was painful, but the S&P 500 reached new highs by 2013. Long-term investors who stayed invested recovered and continued growing wealth.

5. Raiding Retirement Accounts for Non-Emergencies

Withdrawing from a 401(k) before age 59½ triggers 10% penalties plus income taxes. A $10,000 withdrawal could cost $3,000–$4,000 in taxes and penalties, plus you lose decades of compound growth on that money. Use your emergency fund for actual emergencies.

6. Choosing Between Retirement and Emergency Savings Incorrectly

Some beginners skip emergency savings and invest everything. Then a $1,200 car repair forces them to withdraw from retirement accounts at a loss. Build the emergency fund first, then invest for retirement.

Practical Tips to Use the Third Foundation Safely

Start With Employer-Sponsored Plans

If your employer offers a 401(k) or 403(b), start there—especially if they match contributions. Contribute at least enough to get the full match before considering other accounts.

Understand Roth vs. Traditional Contributions

- Traditional 401(k)/IRA: Contributions reduce taxable income now; you pay taxes on withdrawals in retirement. Good if you expect to be in a lower tax bracket later.

- Roth 401(k)/IRA: Contributions are taxed now; withdrawals in retirement are tax-free. Good if you expect higher income or tax rates later.

Most beginners in moderate tax brackets (22%–24%) benefit from a mix. Start with traditional to capture immediate tax savings, then add Roth contributions as income grows.

Automate Everything

Set up automatic transfers from checking to retirement accounts. This removes decision fatigue and ensures consistency. Most people who manually decide each month end up skipping contributions during tight periods.

Rebalance Annually

Over time, some investments grow faster than others, throwing your portfolio out of balance. Once yearly, check if you need to sell some winners and buy more of underperformers to maintain your target allocation (e.g., 80% stocks, 20% bonds).

Increase Contributions With Raises

When you get a raise, immediately increase retirement contributions by 1%–2%. You won’t miss money you never saw in your paycheck, and this accelerates wealth-building without feeling painful.

Avoid High-Risk Gambles

Individual stocks, cryptocurrency, or timing the market rarely work for beginners. Stick with diversified index funds that spread risk across hundreds of companies. According to NerdWallet, 90% of actively managed funds underperform index funds over 15+ years.

Review Beneficiaries and Contribution Limits

For 2025, 401(k) contribution limits are $23,000 (under age 50) and IRA limits are $7,000. Make sure your beneficiary designations are current—these override wills.

Frequently Asked Questions

Q1. What is the third foundation of personal finance?

The third foundation is investing for long-term goals, primarily retirement. After building an emergency fund and eliminating high-interest debt, this foundation focuses on contributing to tax-advantaged retirement accounts like 401(k)s and IRAs, allowing your money to grow through compound interest and market returns over 20–40 years.

Q2. What are the foundations of personal finance?

The foundations are a step-by-step approach to financial security: (1) Save a starter emergency fund ($500–$1,000), (2) Pay off high-interest debt, (3) Build wealth through retirement investing, (4) Save for major purchases and children’s education, and (5) Build wealth and give. Each foundation builds on the previous one.

Q3. What are the 5 foundations of personal finance in order?

- First foundation: Save $500–$1,000 for emergencies

- Second foundation: Pay off all debt (except mortgage) using methods like the debt snowball

- Third foundation: Save 3–6 months of expenses and invest 15% of income for retirement

- Fourth foundation: Save for college and pay off your home early

- Fifth foundation: Build wealth and give generously

Q4. What was the first foundation in personal finance?

The first foundation is saving a starter emergency fund of $500–$1,000. This small cushion prevents you from going deeper into debt when unexpected expenses arise (car repairs, medical bills, appliance breakdowns). It’s not meant to cover job loss—that comes later with 3–6 months of expenses—but it handles most minor emergencies.

Q5. What is the fifth foundation?

The fifth foundation is build wealth and give. By this stage, you’re debt-free (including your mortgage), your kids’ college is funded, and you’re consistently investing for retirement. Now you focus on maximizing wealth-building through real estate, business investments, or taxable brokerage accounts, and you have the freedom to give generously to causes you care about.

Q6. What is the second foundation of personal finance?

The second foundation is paying off all debt except your mortgage. This typically means credit cards, car loans, student loans, and personal loans. The recommended approach is the debt snowball method: list debts smallest to largest, pay minimums on everything except the smallest, attack that aggressively, then roll that payment to the next smallest once it’s gone.

Q7. How much should I invest in the third foundation?

A common guideline is 15% of gross income toward retirement. If you earn $50,000, that’s $625/month. Start with enough to capture your full employer match (often 3%–6%), then increase gradually. If 15% feels unrealistic, start with 5%–10% and increase 1% annually with raises.

Conclusion

Understanding what the third foundation in personal finance truly means can transform how you approach long-term financial security. It’s not about complex strategies or perfect timing—it’s about consistent contributions to retirement accounts, taking advantage of employer matching, and letting compound growth do the heavy lifting over decades.

The third foundation works because it builds on a stable base: an emergency fund that keeps you from raiding investments during tough times, and freedom from high-interest debt that would otherwise drain more money than your investments earn. Once those pieces are in place, investing for retirement becomes the logical next step toward building lasting wealth.

Start where you are. Even $100–$200 monthly contributions grow substantially over 30–40 years. Focus on low-cost index funds, automate your contributions, and resist the urge to panic during market downturns. The third foundation in personal finance isn’t glamorous, but it’s how millions of Americans build financial independence and retire comfortably.